This project seeks to use the power of financial accounting to build important new incentives for companies to take an active role in tackling inequalities for people in workplaces and supply chains who earn less than a living wage.

A living wage is the minimum income needed for workers to afford the basic cost of living. A living wage varies considerably across countries and communities due to differences in the cost of everyday living, but the benefits are consistent across contexts.

A living wage improves employees’ attitudes and loyalty to a workplace as well as their financial security and psychological wellbeing – key elements for healthy social and human capital.

Our current economic model is underpinned by accounting practices that prioritize short-term financial returns for shareholders over sustainable prosperity within planetary boundaries that benefits all stakeholders. These practices, coupled with the perception of wages as costs rather than investments, directly contributes to growing inequality around the world.

Stakeholder capitalism offers an alternative vision where a company’s purpose is redefined to serve the interests of all stakeholders, including employees, suppliers, customers, communities and the planet alongside traditional shareholders. But, if accounting models do not change, this vision cannot be realized.

An Accounting Model to Report on Progress Towards Living Wages

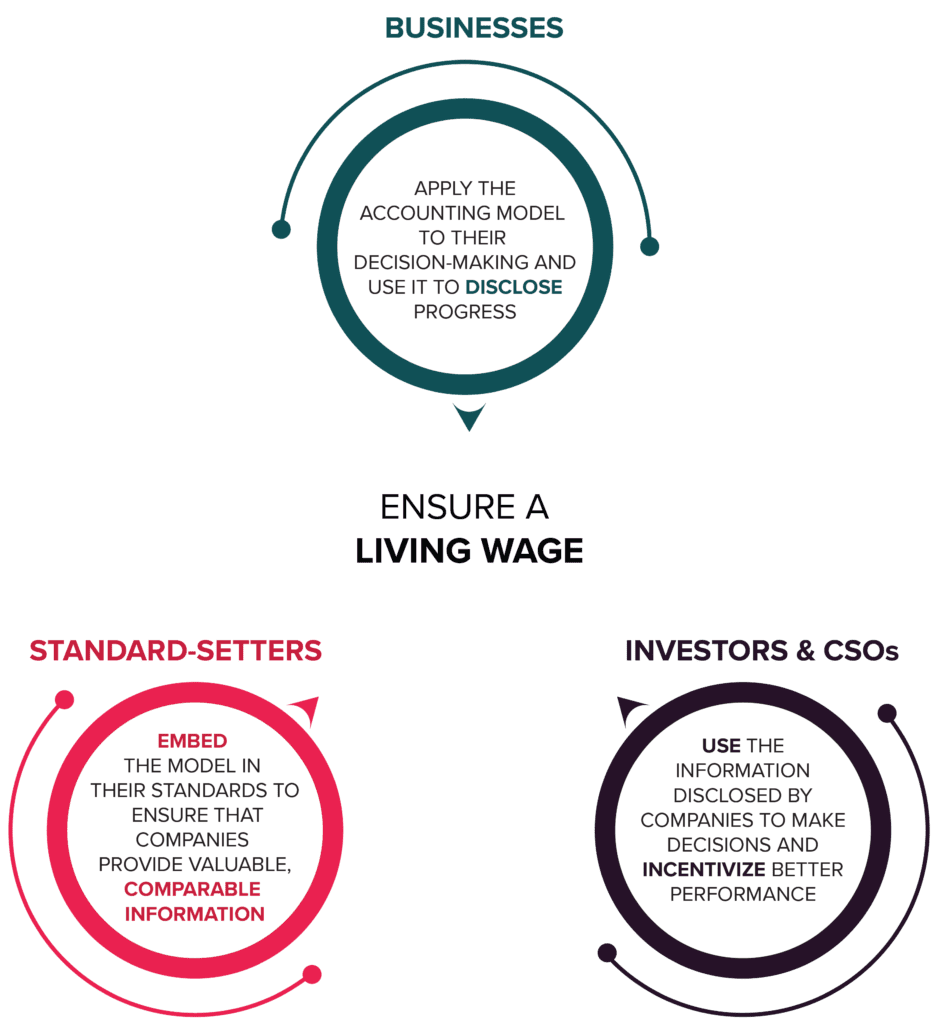

Shift and the Capitals Coalition have joined forces to develop an accounting model that companies can use to measure and report publicly on progress towards living wages across their workforces and supply chains over time. We aim to design a model that helps both businesses and standard setters. For companies, it must help show the value both to society and to the business of living wages. For regulators, it must be capable of integration into accounting and reporting standards, as part of the developments in sustainability disclosures

Methodologies for calculating living wages have been developed and pilot initiatives have demonstrated tangible benefits. However, there is no widely accepted and harmonized model for companies to determine and implement living wage adoption across their operations and value chains.

Post-COVID, we have a critical opportunity and political momentum to address the challenge of growing inequalities, especially among low paid workers whose work has been deemed ‘essential’.

Through an inclusive process of consultation and collaboration, this project will build on existing foundations to develop an accounting model that illustrates incentives for companies adopting living wages.

We are developing an accounting model that can help

The accounting model aims to:

- Enable standardized disclosures in a company’s annual report, much like those for greenhouse gas emissions or the gender pay gap.

- Apply not only to a company’s employees but to its wider workforce (including those in forms of contingent labor) and workers in at least its first-tier supply chain.

- Look not just at the status of workers in relation to a living wage at a point in time, but measure progress over time towards living wages for workers who are yet to reach that threshold.

Why an accounting model?

An accounting model through which companies can publicly disclose the value of living wages can play a catalytic role in delivering greater transparency, informing new standards and creating incentives for improving wages and reducing inequalities. This is essential to rebuild economies that advance human dignity and equality – our social and human capital – across the world.

Progress update: Piloting the beta model with companies

After extensive conversations and consultations with representatives of living wage benchmark methodologies and initiatives, accounting experts, companies and investors (see summaries), Shift and the Capitals Coalition have arrived at a Beta version of the Living Wages Accounting Model, that is now being piloted with companies.

The Beta model metrics are organized under three disclosures:

- The Living Wage Threshold

- The Living Wage Deficit

- Human Capital Erosion

These unique core metrics are accompanied by a broader set of proposed disclosures, which are organized according to the four-part framework set forth by the Task Force on Climate-Related Financial Disclosures (TCFD) and adopted by the International Sustainability Standards Board (ISSB), based on ‘governance’, ‘strategy’ and ‘risk management’ in relation to living wages, in addition to ‘targets and metrics’.

This model is now being piloted by a select group of small and large companies, to assess the viability of the model and the value of the insights it brings. The pilots began in July 2022 and will finish in December. A final version of the model, along with accompanying resources, will be published in spring 2023.

An initial focus on living wages made sense, both because wages are relatively easy to measure, and – more significantly – because a living wage has catalytic power to open the door to the realization of many other human rights.

Caroline Rees, President of Shift.

This project is incredibly important for how companies’ understand the value created by people – social and human capital. By including a living wage in the accounts, we can address one of the biggest challenges of implementation – that it is seen purely as a cost, ignoring the fact that investing in living wages can generate a return for the individuals, the company and society.

Mark Gough, CEO Capitals Coalition

The Accounting for a Living Wage project aims to integrate existing progress towards living wages into a model for companies to account for their performance. Both internally for management decision-making and through external disclosure.

This shift will enable private reporting frameworks to embed a living wage in disclosure expectations, and for public regulators to integrate living wages into standards and legislative initiatives.

Building a living wage into accounting practices is the next essential step to ensure that the benefits of a fair wage are realized. By accounting for a living wage, a basic income will become standardized and will move from being an option for how companies might choose to act, to the way that every business acts. This is essential to rebuild economies that advance human dignity and equality – our social and human capital – across the world.